Get ready for the Statutory Payments increasing in 2025

Each year statutory payments, employment rates and limits increase, this occurs in April each year, all in all the rises

You may have heard news lately that pension funds have been put at risk by the government’s ‘mini-budget’ a few weeks ago. Whilst there has been some fear about the stability of pension funds and it is really a matter for Independent Financial Advisors (IFA), Wealth Management Advisors/Companies and of course pension providers, we understand people may turn to HR to explain what’s going on. Whilst we do not proclaim to be experts we wanted to explain why the panic occurred, what has been done about it, and what action you might need to take in regard to your pension, in all instances we urge you to speak to an expert.

To understand the current crisis, you need to understand what gilts are. Gilt are also known as Government Bonds, and you can think of them as a loan the government can take out with private citizens and businesses. These bonds are bought for an initial investment, called the Principle. They are then listed with two key properties. The first is the Coupon Price. The Coupon Price is an amount of interest the Government will pay on the bond every year. The second is the Maturation date. This is the period when the bond expires, and at this point, the Government will pay the bondholder back the Principle they invested to begin with.

To understand the current crisis, you need to understand what gilts are. Gilt are also known as Government Bonds, and you can think of them as a loan the government can take out with private citizens and businesses. These bonds are bought for an initial investment, called the Principle. They are then listed with two key properties. The first is the Coupon Price. The Coupon Price is an amount of interest the Government will pay on the bond every year. The second is the Maturation date. This is the period when the bond expires, and at this point, the Government will pay the bondholder back the Principle they invested to begin with.

Government Bonds can be used to pay for all kinds of things. You might, if you enjoy collecting vintage things or having vintage prints on the wall, be familiar with the US War Bond propaganda used to encourage citizens to invest in World War II. This is because a lot of the finance for the USA’s participation in World War II came from the buying and selling of bonds. The same is true of our own government – it can use the money it raises selling bonds to pay for war, education, infrastructure, investment – whatever the need of the day happens to be.

So what do gilts and bonds have to do with pensions?

Well, consider this – you are a pension fund manager, and you know in forty years, you will have to begin paying out over £10mil in pensions. You also need to find a way to finance the fund in the meantime, paying staff who will manage those pensions, collecting payments, and so forth. One smart investment can be in bonds. You purchase £10mil in bonds set to mature in forty years’ time. Assuming those bonds have a Coupon Price of 1.5%, you can then sit back safe in the knowledge you have £10mil stored away to pay the pensions off when the time comes, and also £150,000 a year coming in the form of Coupon Payments every year. And because you trust the government to pay its debts, this return on your investment is a very sure thing.

But pension funds like to go further and do something called hedging. This is far too complicated to go into right now and involves many, many financial techniques, but the principle is to protect one investment by balancing it with another. This reduces the risk to the entire portfolio, which is important in an investment as long-term and vital to people’s livelihoods as their pension pots. The difference between a successful pension fund and an unsuccessful one can be many years peace for many thousands of people’s lives.

Unfortunately, many pension funds hedge against interest rate hikes, even though this would generally increase their coupon prices. This has been good for pensions in recent years due to the historic lows in interest rates but given the current financial crisis and the spiralling inflation rate, the Bank of England has been attempting to cool off the economy by increasing interest rates and reducing quantitative easing. The effectiveness of this effort has been debatable, as inflation as of August 2022 still stands at 9.9%, but we won’t get much into it here. The important part to note is that increasing interest rates to cool borrowing and reduce spending is part of the Bank of England’s inflation-reducing monetary policy.

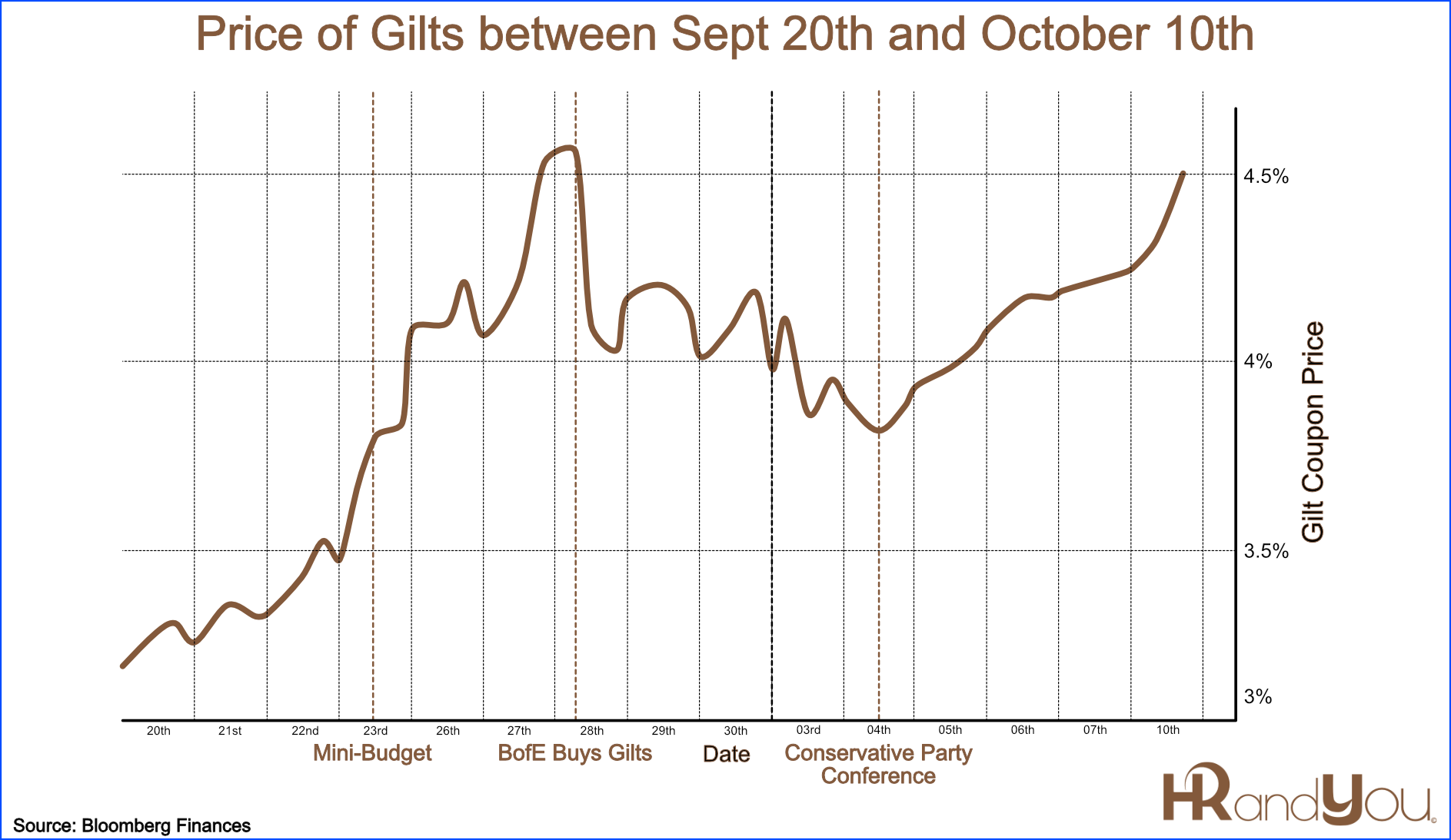

Enter the mini-budget, or Growth plan, released by Chancellor of the Exchequer Kwasi Kwarteng. This plan was a huge shock to financial markets, which instantly began to panic over the budget’s sustainability. One reason for this panic was the complete disregard for the Bank of England’s monetary policy, which was trying to cool the economy, whilst the Treasury released plans to try and inflame it. This was the policy clash equivalent of trying to pour both water and fuel onto a raging fire. Another reason is the assumption that the £60bil black hole in the budget will be filled with bonds, which is causing the gilt market to panic and push prices up and up.

As a result of soaring inflation and the market turmoil inflicted by the completely contradictory and inflammatory budget, pensions were being forced to sell off more and more of the bonds they had bought in order to stay afloat, fueling the rise in coupon prices, and many risked defaulting and collapsing entirely. To prevent this, the Bank of England stepped in and ordered the purchase of the bonds in order to ‘cancel’ them and release pension funds of the burden they bore. As of the 10th October, the Bank of England is raising the limit on how many bonds it is willing to buy in a single day to £10bil, from £5bil. The hope is that more pension funds will take up the scheme and offload their bonds.

For now, this seems to be working, but financial experts are concerned that when the scheme ends on the 17th October. The Bank has suggested that it intends to implement more measures to help protect pensions, such as liquidity insurance operations, but there are concerns that the ‘ticking time bomb’ of mortgages risks the very stability that the Bank of England had hoped to secure with its bond-buying scheme. Many experts feel it falls to Kwasi Kwarteng and Liz Truss to reverse their budget to avoid the crisis.

This situation is continuing to develop, and we can’t say for sure what will happen in the future. Therese Coffey has reassured the BBC that she was “absolutely confident that pensions are safe”, and the Bank of England has reassured markets that they will do “whatever is necessary” to prevent the collapse of the pension market. However, if you are concerned about your pension, you should reach out to an expert in financial planning/wealth management and ask for clarification from them what they are doing to safeguard your savings.

If you need any assistance with pensions, and financial; planning this really a matter for Independent Financial Advisors (IFA), Wealth Management Advisors, and or companies and of course pension providers, we are more than happy to recommend if you do.

Should you need any HR or employment law advice, please do not hesitate to give us a call on 0333 006 9489 or email us at [email protected] and we would be more than happy to point you in the right direction.

This article contains a general overview of information only. It does not constitute, and should not be relied upon, as financial, or legal advice. You should consult a suitably qualified Financial Advisor on any specific problem or matter.

HR and You Ltd, owns the copyright in this document. You must not use this document in any way that infringes the intellectual property rights in it. You may download and print this document which you may then use, for your own internal non-profit making purposes. However, under no circumstances are you permitted to use, copy, or reproduce this document with a view to profit or gain.

In addition, you must not sell or distribute this document to third parties who are not members of your organisation, whether for monetary payment or otherwise.

This document is intended to serve as general guidance only and does not constitute financial or legal advice. The application and impact of laws can vary widely based on the specific facts involved. This document should not be used as a substitute for consultation with professional financial, legal or other competent advisers. Before making any decision or taking any action, you should consult an expert.

In no circumstances will HR and You Ltd, or any company within HR and You Ltd be liable for any decision made or action taken in reliance on the information contained within this document or for any consequential, special or similar damages, even if advised of the possibility of such damages.

Each year statutory payments, employment rates and limits increase, this occurs in April each year, all in all the rises

This year as an Employer you need to be aware the potential for a shortfall in annual leave entitlement for

What should you do when someone resigns??, a quandary that perhaps you have faced, are facing, or will do in